Charging our kids rent dilemma

I stumbled upon a Reddit thread the other week which got me thinking:

Should we charge our children rent?

As financial independence seekers, it would seem obvious to charge our children rent. It might seem like a ruthless side-hustle, but hear me out here.

I set up an impromptu 24 hour twitter poll which reached 2,875 people and 91 people voted.

Read a thread on reddit about parents kicking their children out at 18 to save money or charge rent whilst they are still in high school.

Is this a cultural thing or a socio economic thing?

As FI seekers, do you charge your kids rent? If so, why?

No judgement. Curious.

— Cashflow Cop (@CashflowCop) May 12, 2019

I expected this to be divisive, but turns out not as much as I thought.

As I mentioned in my tweet, there are perhaps cultural and socio-economic factors to consider but I won’t be going into those here.

I’m going to be purely looking at this from the FIRE lens.

I will also assume that we will not need the income from charging our kids rent.

What I will say though is: there are families out there who are in some really bad financial situations. As soon as their children turn 18, they see their parental responsibility to provide as over and charge them rent. Sometimes charging them rent even whilst they are still in school.

This article makes no judgement.

In this post, I am talking about anytime from the age of 14 (the legal age to work in many countries). So this isn’t just about adults, but includes children. Just not too young though…

If I had kids, I would shake down their diapers for coins…

— Lisa (@alawyerhermoney) May 12, 2019

(To be clear, Lisa is joking) – apparently she wasn’t joking 🙂

This is more of a thinking out-loud type of post. I will wear two hats and attempt to argue for each opposing side before concluding with what we will likely end up doing with our own children.

Lets keep it simple

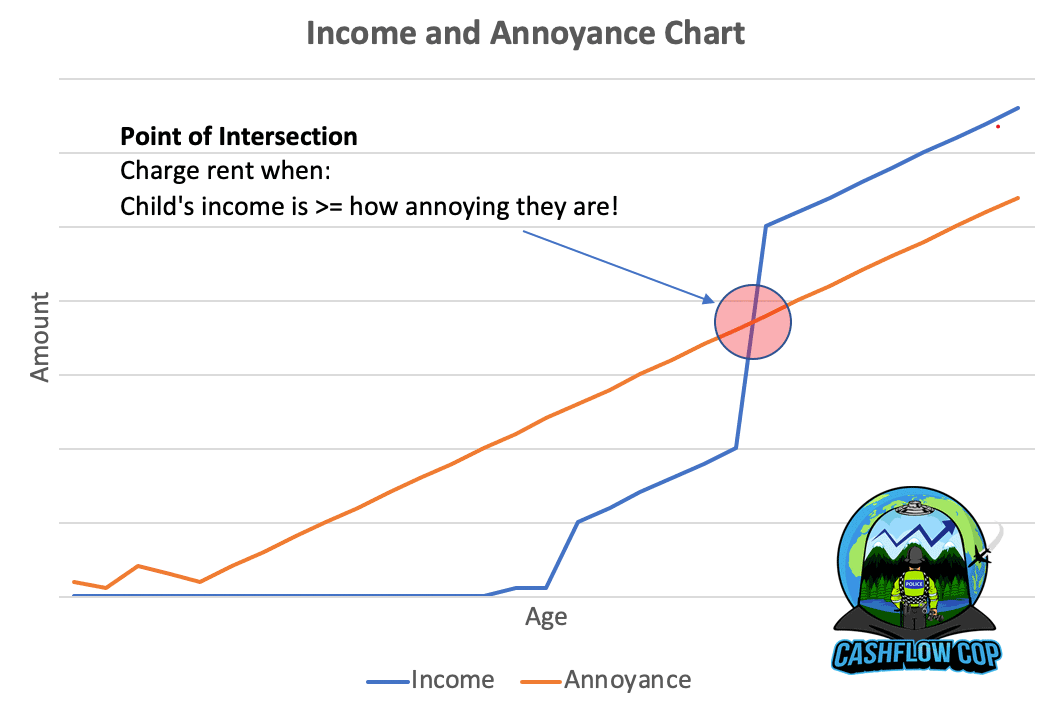

Before I begin, I thought about keeping things simple and not to overthink this.

The chart below illustrates how I could decide on the right moment to charge our kids rent.

What we could do is plot as our our children age how annoying they are and how much income they earn. The point at which their income reaches how annoying they are is when we should begin to charge them rent.

‘Simples’ right?

Maybe I should stop here and end the post.

In all seriousness, let me put a bit more thought into this…

Why I’ll charge my kids rent

Responsibility was cited a number of times as a key reason to charge children rent. Making them financially responsible for having a roof over their heads, even if it were only a token amount will force them to grow up and understand that life is not a free ride.

From the age of 14, many kids can start to earn money. They might even get pocket money. So charging them a fraction of this could teach them to be responsible.

I’ve seen far too many times, especially in my work how spoilt children can end up relying on their parents for life, or worse on the wrong side of the law. Charging them rent early on will slowly teach them to be responsible for themselves rather than wait until they are 18 and expect them to change with a flip of a switch.

The amount of rent charged could increase based on their age and how much money they get through work or pocket money.

Financial skills like budgeting, self-discipline and frugality might be developed if they know that at the end of the month, mum and dad want their rent. Of course, I will be there to teach and guide them. However, instead of something abstract and theoretical, the fact that they need to pay rent provides something tangible for them to understand and learn.

Extra money is aways welcome, especially for a family on a below median household income with other costs like childcare to contend with. Even if the family does not need the money, is it only fair that a teenager starts contributing financially?

This is where people start to have strong opinions.

Imagine my 16 year old kid starting his first proper part time job. He makes £500 per month tax free working in retail or hospitality over the weekends. Despite my efforts, he spends all his money on fancy footwear, clothes and games.

He saves nothing.

His studies are okay, but could be better if he focused more on school and less on working.

Come Mondays, he is now tired and starts to fall asleep during lessons.

Surely it is morally acceptable for me to charge my son a small amount for rent? Maybe it will make him value money more. Perhaps it will cause him to work a little less and focus on his studies instead.

We have another child so the extra money we collect from him could help towards school tuition for both of them. It could also be saved to go towards their first home or university fees.

Emotional strength is another reason I’ve come across for charging our kids rent. There is something to be said about ‘tough love’. To place them outside of their comfort zone. Add a bit of healthy stress in their lives to not only financially but mentally prepare themselves for the real world.

Gaining independence and confidence because our kids are learning and developing all of the above points early on in life. If we were to give them a free pass to live rent free with us for the rest of their lives, where is their motivation to grow-up and to be independent adults who add value to society?

Why I won’t charge my kids rent

Education is an important part of our family. I grew up where our parents kept reminding us of this and how we should not waste the educational opportunities that are available in this country.

By charging our kids rent, it will act as a distraction to their studies. They may grow to love the idea of earning money more so than studying. This may be the spark which causes them to drop out of school. At this age, we would want studying to be a priority over earning money.

Their childhood should be maintained. Even at 14 years old, I worry that by charging them rent, no matter how small, I will be robbing them of the last remaining childhood years to be care-free.

Do I really want my 14 year-old child to worry about paying us rent? Despite how light-hearted, educational and fun I make it, some kids are natural worriers. I might be forcing them to grow up before they are ready to.

Resentment can build up within their minds. When they compare themselves against their peers, they might be wondering, why are my own parents charging me rent?

This feeling could be minimised by taking the time to explain to them, but doubt can creep back in. Kids can be easily influenced at that age.

Our relationship could change. Everything we do as family ends up having a monetary value attached to it. If we wanted them to help out around the house above the usual, how would I react if they turned around and said: “can I have a reduction in rent this month please?”.

If I wanted them to look after their younger sibling for the evening, they could demand payment for doing so.

This change in mind-set and the relationship between parents and children could be very difficult to reverse.

Love and support is the most important consideration for us. I guess all the above points could be grouped together under this heading.

Would charging them rent make our kids feel like we love them less?

Would it go against the idea of being supportive parents?

It could be argued that all of the positive points of charging them rent are in themselves proof that we love and support them. It’s just done in a different way, but I need to accept the risk of how our relationship with our kids could change.

Why I’ll just kick my kids out

There is also another, more ruthless option.

Just kick our kids out.

I am talking here about once they are done with their education and are adults.

If they know there will always be a free place for them to stay, they might become less motivated individuals. Believing that after a certain point in their lives, mum and dad will charge them rent if they want to flee back to the roost will make them think twice about taking the foot off the gas in making a life for themselves.

What will I do?

The little thought experiment above was fun to do. Forcing myself to view this from different perspectives even if I didn’t believe in them. It has really helped me to decide what might be best for us.

It’s important to remember that every parent, just as every child is different. I am not sure there is a right or wrong in all this. The key thing is the motivations behind the decision.

Are we acting in our children’s best interest when we charge or not charge them rent?

I think that’s the main question we will ask ourselves when it is our time to decide.

Growing up, my parents did not charge us any rent. Even when my younger brother moved back home after studying and his girlfriend at the time joined him, they still didn’t charge them rent. My brother and his girlfriend contributed towards household bills, but they chose to do that. They didn’t have to.

Also, there was no such thing as payment for doing housework when I grew up. We either helped out as asked or get a telling off (sometimes punished) if we didn’t.

I didn’t get pocket money until I reached secondary school (11 years old). I would get £0.50 per school day from my parents to help top-up our free school meals (we were classed as low-income), grab a snack at the tuck shop or get a bag of chips on the way home. Later, my parents increased this to £1 and then eventually to about £2.50 (includes my bus fare).

My experience growing up has shaped my views to where I am leaning more towards not charging our kids rent.

I particularly like this idea:

But I also like the idea of collecting rent, so they learn the responsibility and costs of being an adult, but saving that up for them to help them when they leave the nest. That way they can leave with an Emergency Fund already in place, or start investing in their retirement

— Josh Overmyer (@Jovermyer1) May 12, 2019

So this is what I think we will end up doing:

- As long as they are in full-time education, we will not charge them rent (yup, this includes PhD if that is what they choose to do).

- Once they finish their studies and need a place to stay, they will always be welcome to stay with us rent-free so long as they are actively looking for work.

- As soon as they find a job, they can still stay with us to help them save and find their feet. However, they will contribute towards household expenses, including rent.

- Again, we will keep this money separate and invest it for them. We will gift this back to them as and when we feel the time is right.

This feels like the right balance to us.

My aim with my children is through watching us and listening to everything that we will try to teach them, they will become financially literate. More so than I was when I was a teenager.

I hope that they would want to save and invest from the very first pay cheque.

The risk of damaging our relationship by adding an extra layer of precaution in the form of charging them rent (and investing it for them) is more than we are able to accept.

I’d like to give them the freedom to grow up knowing that as parents, we have brought them up to be the best they can be. We will be there to support them and trust them to pick out our best traits as their forge their own way in life.

My eldest is still only two, so I’ve got some more time to think about this.

So over to you:

What do you think about this?

What was your experience growing up?

More from the Blog

Investing for Our Children: Will it Ruin or Motivate Them?

My Property Investment Journey – Part 1: Making £100k with Lodgers

Humans of FI

Amazing thought experiment! I’m not sure if I would ever do this, but then again I’m a long way from having kids.

I do see how writing this article benefitted you, by being forced to look at the problem from both sides you made it really clear.

Also, I loved the idea of Josh Overmyer, charging them rent but then saving/investing it to help them out when to move out. It can really kickstart their life, for example by being applied to their student loans, the down payment for a house, or a first lump sum investment into their retirement accounts.

It was fun to write!

The thought of charging them, but actually investing the money instead never crossed my mind until Josh suggested. Seemed so obvious once he mentioned.

Sometimes the simplest of ideas get overlooked when we over-think things.

Interesting to read your thought experiment, CfC. Your kids are still so young though so plenty of time for you to change your thinking when the time comes!

As kids, our pocket money was linked to chores around the house. If you didn’t do your share, you didn’t get a penny so I learned at an early age that ‘work paid’…

As an adult, as soon I got a full-time permanent job while I was still living at home, my mum asked (no, demanded!) that I pay towards food and bills. She didn’t need the cash but I didn’t argue. I paid around �50 or �60 a week which was probably on the high side back in the 90s and was around 25% of my then salary. However, this did mean that when I eventually got my own house at the age of 30, I was already used to shelling out an amount regularly for bills, so more good than harm was done in that respect.

As I said, my folks didn’t need the money but perhaps it went towards their own early retirement!

It�s interesting to hear your pocket money was linked to chores. It was the same for many of my school friends.

I remember my parents mentioning it once when younger after hearing it from somewhere. They dismissed straight off the bat. They were very traditional in their thinking. Less so now. But their view was that, as their kids, we do as we are told and should not be rewarded for helping around the house.

�50 a week definitely sounds a bit high for the 90�s. I would expect lobster dinner once a week with that rate!

You�re right though. I suspect my view will change over time. I might turn into right softie, or at the other extreme, be militant like my parents. I�m hoping for somewhere in between. I already give my two year old too many treats – I can�t help myself. He has such a cute little face and wonderful smile!

This issue is a tricky one to get right, with lots of hidden traps whatever you choose.

Speaking as someone who was on the receiving end of such an arrangement, it will irrecoverably alter the relationship between a child and their parents. The unconditional (in an ideal world) love and support children hopefully take for granted in the family home now has (more) strings and a price tag attached. There is no way to put that genie back in the bottle.

If the goal is to encourage the child to leave home then it can prove very effective. If not, then beware of a financially savvy kid shopping around and obtaining a better deal elsewhere.

While this is probably good for them in terms of growing up and becoming self sufficient, it may not work out exactly as intended. For example living with an older boyfriend can be more cost effective than having to pay rent to a landlord.

Even if the monetary aspect of the arrangement is affordable for your kid, they will no doubt also weigh up the other “rules” that come from remaining in the family home and wouldn’t exist if they lived elsewhere.

Babysitting younger siblings.

Chores.

Curfews.

“Duty job” family visits.

Not being allowed to have friends couch surf, hook up, play loud music, smoke drugs, etc.

It is also worth observing that your proposed system potentially disincentivises the child from leaving school or finding a job. They experience a free ride until commencing work, then potentially makes them feel punished for seeking employment (rational or not). Even if they knew they would (probably) receive their “rent” back as a gift at some indeterminate date in the future, they are still without the money today.

Perhaps this is what some academics might call a ‘wicked problem’; one where there is no perfect solution.

“Irrecoverably alter the relationship between a child and their parents” is my main concern.

Based on your comment about being on the receiving end of such an arrangement; what I am hearing is that from your experience, the negatives outweighed the positives? If you don’t mind sharing, how do you, or are you planning to navigate this?

I’m lucky to have some more time to ponder over this.

> the negatives outweighed the positives?

It is important for the parents to have thought through the possible consequences, and be aligned in their desired outcomes. Children may not respond as anticipated, potentially causing rifts or making life harder for those left behind. Families are complicated.

> If you don�t mind sharing, how do you, or are you planning to navigate this?

I think it is an extension to the approach parents adopt to pocket money. I wrote about my approach here, things don’t always go to plan!

On the housing front, we’re encouraging our kids to go away to university, hopefully including a stint overseas (exchange year or full degree). The confidence and life experience gained by travelling and fending for yourself is both rewarding and invaluable. Whether they are ready, willing or able remains to be seen.

They know there is always a place for them at home if they need it. That said, I’d be disappointed if they didn’t make their own way in the world once they’ve finished school.

I can�t imagine an adult post college child wanting to live at home with their parents. And we would not have allowed any of our three to do that unless there was some special circumstance like an illness or for a brief time between changing where they live from one city or state to another. Visits are great, we even keep their pets if they are traveling, sometimes. But just to save them money for an extended time period, I wouldn�t want to risk damaging their growth into fully independent adults by doing that.

I imagine that is certainly true for most. The last time I lived in the family home was when just after I turned 18, the night before my parents helped transport all my belongings to university halls.

To move back and lose my independence would be just too much.

I guess as parents, one of the worries we might have is that our children rely on us for the rest of their lives. They end up living with us as adults because they can’t get out of their comfort zone. I have seen this happen. Actually, this person (in his 30s) is still living with his parents now!

It’s such a difficult balance. To be supportive but at the same time nudge them enough so they have the confidence to make their own way in life without negatively impacting the parental relationship.

I’m 28 turning 29 soon and only now looking for my own place, however because my parents never charged me “rent” and I have a decent relationship with them, i.e., I help around, buy my own food and listen to them when they ask or suggest something, we have no issues at all.

Because of that I was able to save a good amount and invest the majority of my income. My investment is about to reach 100K and I can look at for a decent house I can immediately move into with no work required.

The thing is, they never gave us things just like that nor did we get expensive stuff.They taught us to be mindful of what we spend and save everything we get since materialism is never going to really satisfy you.

If they charged me, I would just stay longer.

Thanks for sharing your experience Mr. Fight to Fire.

You�ve managed to save an impressive amount.

It�s interesting that you say if they charged you rent, you would have actually stayed longer. Presumably because it would have meant you needed more time to save the desired level of deposit. Some have reported the opposite effect where it actually made them want to leave the family home sooner.

It goes to reinforce my personal view that every parent and child relationship is different. Even with a well thought out and well-meaning plan, sometimes you just gotta go with the flow. So long as I tried my best to think things through and be intentional about it, then hopefully it will all be �okay� even if it isn�t �perfect�.

I think charging your kids rent whilst they’re still in full-time, compulsory education is a bad idea. If nothing else, I’d rather my (theoretical) kids were studying, so they could get decent jobs and look after me in my old age!

I left home at 19 to go to University, so I haven’t ever had to worry about paying my parents any rent. However, my brothers didn’t have the same idea, and stayed living with my parents until their mid-20s. I think my parents started charging them rent once they finished University. Despite this, my brothers still had part-time jobs during this period. It allowed them to splash out every so often, whilst saving up a deposit for a house.

I think doing this avoided the impact on the parent-child relationship that Indeedably described above. By the time they had to pay rent, they were independent adults anyway, keen to make their own way in the world. It just so happened that living rent free for a few years (and then with below-market rent after uni) enabled them to save up a deposit fairly quickly.

Having said all that, I wouldn’t trade my own experience for theirs any day of the week. Living away from home for Uni, and then working abroad for two years afterwards, gave me a level of independence and experience that I would not have gotten if I’d stayed with my parents. So I’d echo Indeedably’s comments in encouraging your kids to leave home. Of course, who knows what University fees and rent will be when the time comes!

It�s really interesting to hear different opinions on this and the reasons.

Like all best laid plans, chances are, it�d go to sh*t when our children cause us to think with our hearts instead of our minds…but is that really a bad thing? Only time will tell.

I�m with you on the education thing. So long as it has the potential to help them secure a decent job. A degree in left-handed puppetry, regardless of how passionate they might be about the subject just isn�t going to cut it. The price of that is full market rent I�m afraid.

I’m in the position where I currently don’t have any children (late 20’s) and still undecided whether or not to have any! But many friends who do have children say practically the same thing – past the ages of 13 till 18 is supposedly the hardest stage of it all (which I think that graph perfectly sums up that level of ‘annoyance’ :D!)

Haha. My kids are far from 13, but I guessed that it might be the case so drew the graph that way. Might as well manage my own expectations.

Pingback: The Full English – Student Loans Review – The FIRE Shrink

Oooooh. This is a good one 😉

My kid is 4, so she still doesn’t quite understand the concept of money. She has a piggy-bank, and whenever we go to ANY shop, she wants something. And we sometimes cave in, but for the most part we always say: If you feel you can’t live without this item (although you already have 1000 teddy bears at home), you can buy it – with your own money. She never bring her money, so we’ll have to come back to the store WITH her money. It happens maybe 1/10 times that we return (another day) and bring her own money. This means that there’s never actually more than �10-�20 in her piggy bank. We don’t give her any money. The money in her piggy bank is typically from the grandparents.

When I was a kid I always had money somehow. I never received an allowance, and it has happened a number of times that my parents borrowed money from me (we were not poor, but I think they were struggling a bit for a while). I never asked what they needed it for. I was maybe 11 or 12 years the first time it happened. It was �200, and I had maybe �1000 in my bank account at that time. I didnt charge them interests though (damnit), as I didn’t have THAT much financial savvy back then 😛

The money that I had in my bank account (and my pockets) came mostly from gifts and the occasional �10’er from the grandparents (or great grandparents). I was such a scrooge, and my grandparents still remind of that to this day 😛

I’ve been giving this a lot of thought, and I really believe that money and love should NOT be tied together. The fact that you would charge your kids rent has nothing to do with whether you love them or not. Money is (should be) just a natural part of life, as common courtesy, looking for traffic before you cross the street, or being polite when you meet new people.

My goal is for my 4-year old to become financial litterate, before she gets her first job. This way, I won’t have to teach/force/tell her how to treat money. BUT, the law dictates that you’re not your own “man” before the age of 18. – So let’s imagine she gets her first job when she’s 14. I hope she is going to do the right thing (save at least 25% of what she earns), but if she doesn’t, I OWN her ass, so I’m damn well going to force her to do that (parents have control of their kids bank-account until they turn 18). She will have to learn early in life that any money you earn, you only actually own 75% of (give or take). The rest is for the “tax-man”. Somebody has to pay for the roads, the benches, the gartners, the athletics department and the schools (this I will make damn sure to teach her 😉 ). In Denmark you can earn �4000 as a minor, without having to pay taxes. When you turn 18 this amount is raised to about �5500. So, if she earns less than this, she will get to keep those ~25% for herself – but ONLY if she doesn’t spend them (this is what I’m going to teach her) 😉

Having said this, I feel the need to also point out that we (me and my wife) swore that our kid would not become an Ipad kid. She knew how to operate that thing before she turned 2, so that didn’t pan out very well! HAHA! At least we managed to keep the rule of “no Ipads during dinner” 😉

How do I plan to teach her about tax then? Well, so far I’ve worked up the idea for her to have 2 piggy banks. Whenever she gets �10, she will be required to put �2.5 in her “not-to-be-used/tax” piggy-bank. This way she will start saving early in life, and getting used to never receiving 100% of what she “earns”. She might as well learn now! (I haven’t installed piggy-bank #2 yet, but I plan to do it before she starts school next year). This will also give me the opportunity to teach her about compound interest, by offering to add an additional �10 for every �100 that she saves in the “not-to-be-used/tax” piggy-bank (gonna test that marshmellow effect, haha!).

About your plan, I have a few comments:

1. As long as they are in full-time education, we will not charge them rent (yup, this includes PhD if that is what they choose to do).

2. Once they finish their studies and need a place to stay, they will always be welcome to stay with us rent-free so long as they are actively looking for work.

3. As soon as they find a job, they can still stay with us to help them save and find their feet. However, they will contribute towards household expenses, including rent.

4. Again, we will keep this money separate and invest it for them. We will gift this back to them as and when we feel the time is right.

I think this is the approach that most “modern parents” would take. However, I believe this “plan” to be faulty. I understand the dilemmas about not wanting them to “rush through education”, or to QUIT education altogether to work instead, but it all boils down to my initial statement, of money being a natural part of life – and whenever you receive any money, you don’t own 100% of it. It’s that simple. WHO gets the part that you don’t own, is a different matter.

My parents divorced when I was 3 years old. They both remarried a couple of years later (they are still together with their respective spouse to this day). When I was 10, my dad got another son (my halfbrother). Giving the story that I told above (with my parents borrowing money from me) it was quite clear that my parents didn’t have to teach me how money works – I somehow already knew. To this day, I still can’t quite quantify what gave me the “money accumulation abilities” – it seems I was just born with them, somehow. I could hope that my kid would grow up to share this ability, but so far I’m not seeing any signs of this 😛 (with the chance of being flamed by the female mob, I sense that most females have a tendancy to be a bit more frivolous with their money, than their male counterparts – but that’s just my perception!).

Anyway, long story short (too late!), my younger brother was brought up in a similar environment as me; no chores, no allowance and no restrictions (spoiled brat). He also somehow managed to get the money-gene (maybe it came from my dad?!) – but his mother demanded he “pay rent” when he got his first job. He got two options:

1. Transfer xx% of his earnings to his parents (which they would then save and gift him later, like you plan) OR

2. Put xx% of his earnings into a (his own) savings account, which he could not use until the day he moved out of the house

My brother and I both planned to live at home until we finished our university degrees and got our first job (it was cozy, and cheap). I moved out when I was 19 (because I found a girlfriend who already had her own place in the city).

My brother stayed the course, and stayed with his parents until he finished his education and got his first real full-time job. Because he had chosen option 2, he had accumulated enough money for a down payment on his own apartment (2 bedroom – that little scrooge!). He got his own place when he was 22, I got my first place when I was 27.

So you see, your option 4 should be: MAKE them (if they don’t do it voluntarily) set aside 25% of their earnings, and TEACH them how to invest it. – Don’t invest it for them, they won’t learn anything from that 😉

My kid is (I hope) going to be a regular Warren Buffet by the age of 18! (fingers crossed that it doesn’t turn into another Ipad-situation!)…

You win the award for the most epic comment on the internet today!

Thank you for taking your time to write that.

“Money and love should NOT be tied together.” – I love this. The difficulty is, children being young and they say our adult minds don’t mature until at least our mid 20s, can they: 1) understand this; and 2) accept it.

We’re in the same position as you. We’ve always said that our kids will not be using Ipads. My two year old can use it better than me! Although we are restricting its use to only nappy change time (little dude won’t stay still) or when we need 10 minutes to recover. It’s easy to judge until we had kids ourselves.

That’s an interesting story you’ve shared. It sounds very much like you and your brother just ‘get it’ when it comes to money. Most need more guidance, which is something I am definitely going to do with our kids.

We intend to invest for them and teach them what we’re doing until they are old enough to understand and do it themselves. I see your point in relation to option 4. I’ve got plenty of time to tweak this plan. In any case, like most plans, they seldom work out as expected. I might just go with the flow, but at least I’m giving it some thought.

This is an interesting concept/post!

I totally get the idea of using this tactic as a way to teach financial literacy. Learning to budget with small dollars at a young age will pay huge dividends of the course of their lifetime!

Thanks for stopping by Nate. I think I’m still on the fence with it all. It’s about weighing up the pros and cons, then deciding what is best for my family and most important, the individual child.

I am going through a situation that fits this topic perfectly. I am 27 and I didnt make the best choices so far ending up back at home. To be honest I’m a recovering addict and I just had 1 year on Feb 1st but anyways ive been living with my parents and it seems like every time I get money she expects me to give her some, sometimes even taking all of the money I earned. I have to pay for my gas when I use her car which I dont mind but then I have to pay for her gas too. I’m starting to resent her…i dont even want to be around her cause all she does is complain and I dont get much money..its really hard trying to find a job with no work experience and having a criminal record… And I love the fact that I can actually have money and go buy stuff in stores instead of spending it else where on bad things but I cant even try to save money…if I did she would just end up with all of it anyways so I sometimes even try to spend it as fast as I can so then I dont have it for her to take. She guilt trips me and I just cant wait to move away from her but I dont k ow how I could ever get on my own feet with the way she is about money. Just thought you might want to hear someone as the childs thoughts. Yes resentment is big and I dont feel loved unconditionally.

Congratulation on being one year clean. I�m sorry to hear about your situation. I hope you keep trying so that one day things will be better for you.

Thank you for this article. I wish I had been raised to feel like I have a safe space in the world to return to. I started working when I was 14 and moved out as soon as I was 18. Now I am 28, last year I got a chronic infection of the central nervous system and lost my ability to even walk. On top of that, I am a live sound engineer by profession and because of the coronavirus I have lost all possibility of work within my field. We (me and partner) returned home to live with my father for just a few months while we get back in our feet but it wasn�t long until he started bringing up the subject of rent. I really disagree with the sentiment that letting kids live rent free is �enabling� them to be lazy, it just means you give them a sense of belonging and security in the world. If your children don�t feel like they have any safety net to fall back in it will likely make them much less risk averse, which could affect their future earning potential but more importantly long term happiness. I�ve been spending a long time on the internet and it seems like most people quite callously think �demand rent!� but you really summarise it in this article, that is should be what�s the child�s best interest at heart to motivate whether you should charge them rent or not, and it�s made it very clear who has been in the wrong in this situation. I would never make my future child pay rent if they are recovering from a serious chronic illness, no matter how bad of a financial situation I was in myself (fathers income was also affected – temporarily – by corona, but his income is still 4x that of what mine is currently) it would never seem ok to suddenly rely on my child to top up my earnings in such a situation.

I�m sorry to hear about your situation and thank you for sharing your story.

You�ve summed up my own personal view well. I don�t think charging rent is always bad or equally not charging rent would automatically bring up lazy children. It�s far more complex than that. It depends on two important factors which has to be considered: the parent�s situation and that of the child. Tension, resentment and misunderstanding can sometimes be overcome through open dialogue and communication to understand one another�s perspective. I recognise this is not always possible depending the the parent/child relationship.

(By child, I am referring to adult children)

This is definitely a hard one. I had a very traumatic childhood and do not have a good relationship with my mother. My father did step in and help. He allowed me to live with him while I went to nursing school but I did have to work and pay him $100 a month. This was difficult but I had learned early on to be able to dissociate when things got hard and turn into a machine and just go and do what I had to do. This did help me to become self sufficient but at some what of a cost I guess. I�m now a nurse and a mother, and I look at things a lot different. Since I never felt like I had a real �family� or unconditional love, or a safe place to go when times were hard, I want that for my kids and I want them to always feel at home with me, no matter what happens in life. I always want them to have a safe and peaceful place to come to where they feel at home. The world out there is tough. There�s going to be struggles and hardships they will have to face but not at m house. I feel like I wouldn�t have the emotional and psychological problems i have today if I would have had that. What else is there but family at then end. I want and encourage my children to be independent and self sufficient but I also want them to have a safe haven they can come to when they need to.

You�re right. There is a balance. What is the right balance depends on the individual relationship between parent/s and child. Unfortunately, no one is perfect. Even with the best of intentions at the time, no one really knows the long terms effects on the relationship until it is probably too late.